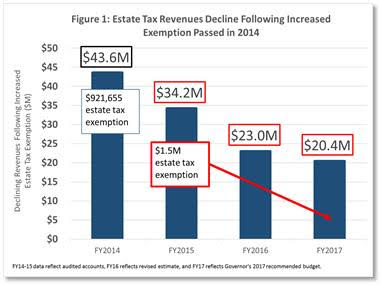

This report comes at an opportune time for Rhode Island, just a week after learning that policymakers are considering increasing Rhode Island’s estate tax exemption from the current $1.5 million to $2 million, a move that would benefit the heirs of fewer than 100 estates.[1] As seen in Figure 1, the increase in the estate tax exemption enacted two years ago already has significant negative impact on state revenues.

This report comes at an opportune time for Rhode Island, just a week after learning that policymakers are considering increasing Rhode Island’s estate tax exemption from the current $1.5 million to $2 million, a move that would benefit the heirs of fewer than 100 estates.[1] As seen in Figure 1, the increase in the estate tax exemption enacted two years ago already has significant negative impact on state revenues.

As Rachel Flum, Executive Director of the Economic Progress Institute, notes, “We face a choice: we can either invest in the things that help our communities thrive and all of us prosper, or hand yet another tax break to a few of our state’s wealthiest people.” Changes to our estate tax have already compromised our ability to make critical investments in the Ocean State. Increasing the estate tax exemption from $1.0 million to $1.5 million in the 2014 General Assembly depleted revenues by $8.4 million in 2015 and by $6.1 million already in 2016, according to the Department of Revenue.[2]

The CBPP report, State Estate Taxes: A Key Tool for Broadly Shared Prosperity, calls on states that have repealed their estate taxes to reinstate them, and suggests that the eighteen states that have estate taxes in place (including every state in the Northeast except New Hampshire) consider improving them. At $1.5 million, the Rhode Island estate tax exemption falls midway between the $1.0 million exemption in Massachusetts, and the $2.0 million in Connecticut.

The CBPP report emphasizes three compelling public policy purposes that result from estate taxes:

- Providing revenue for investments that promote a strong economy. Estate tax revenue supports services that make a state an attractive place to do business and live.

- Reducing inequality. The vast majority of taxpayers would never owe estate taxes. These taxes are paid by a small share of very wealthy families — those most able to afford them.

- Taxing income that would otherwise escape state taxation. Without an estate tax, many unrealized capital gains go untaxed at the state level. This happens when an asset that has increased in value is not sold during the owner’s lifetime, leaving the heirs to gain the profit.

Report author, Elizabeth McNichol, emphasizes the price we pay when we erode state revenues:

You can’t get something for nothing. States that have reduced or eliminated their estate taxes have less money for public investments, so they are seeing higher tuition at public colleges; cutbacks in teachers at K-12 schools; and deteriorating roads, bridges, water treatment facilities, and other public infrastructure.”

Important investments in tens of thousands of Rhode Island’s low- and middle-income working families – such as increasing the state earned income tax credit to 20 percent of the federal credit, and helping families pay for child care–should take priority over tax breaks for a few dozen of our wealthiest families. These investments are particularly important given Rhode Island’s overall tax system, which is “upside down”. The more money you make the smaller share of your income you pay in state and local taxes. A robust estate tax helps to reverse that upside-down tax system, as do changes at the lower end, such as increasing the state EITC.

Douglas Hall, Director of Economic and Fiscal Policy at the Economic Progress Institute notes that “Preserving the estate tax at its current levels gives us revenues needed to give Rhode Island working families a boost, strengthen our economy, and invest in education and infrastructure, while making our tax structure more fair, and preventing those most able to pay from avoiding taxes on their accumulated assets.”

[1] Based on the most recently available data, after reducing by more than half the number of estates subject to the estate tax via changes adopted in 2014, only about 86 filers would remain, 39 of which would see their estate tax completely disappear if we were to raise the exemption to $2.0 million

[2] Revenue projections from the estate tax, seen in Figure 1, incorporate the revenue impact from changing the exemption level, but also reflect the number of estate tax filings, which vary from year to year.

]]>In “It’s Time for States to Invest in Infrastructure,” CBPP Senior Fellow Elizabeth McNichol urges states to make sound infrastructure investments. Now is the time for states to reverse years of decline and step up investment in state-of-the-art school facilities; up-to-date water treatment plants; better highways, railroads, and ports; and other public infrastructure — which is vital to creating good jobs and promoting full economic recovery.

The Center on Budget report places Rhode Island third last among all states (ahead of only Michigan and New Hampshire) for total state and local capital spending as a share of state gross domestic product in 2013 (the most recent year for which 50-state data are available).

Here in Rhode Island, years of neglect have resulted in consistently low ranks on infrastructure such as roads and bridges – more than one in five bridges in our state is structurally deficient according to the American Society of Civil Engineers, and 41 percent of our roads are in disrepair, compromising public safety and costing motorists nearly half a billion dollars a year in additional transportation and repair costs. This state of disrepair should come as no surprise – since 2000, Rhode Island has ranked in the bottom three for state and local capital outlays as a share of GDP in ten of the twelve years for which we have data.

Since 2013, more infrastructure investments have been made. In 2015, the General Assembly approved a five year, $3.4 Billion Capital Budget, heavily weighted towards investments in transportation (43.2%) and Education (17.9%), spanning investments in K-12 schools, higher education facilities, as well as vocational schools, and the School Building Authority was created to oversee the process of overhauling the state’s crumbling school buildings.

The Governor’s 2017 budget proposal recommends significant further capital investment such as in Rhode Island’s public colleges, for affordable housing, and for the “Rhode Works” overhaul of the state’s transportation infrastructure. The recently passed Rhode Works legislation provides much-needed investment to fix Rhode Island roads and bridges and underscores the importance of raising sustainable revenue to ensure that our transportation infrastructure is well-maintained and safe for those who use them.

Modernizing Rhode Island’s transportation systems and other infrastructure boosts productivity by supporting businesses and residents, improving the education and job readiness of future workers, and helping communities to thrive. Investing in our infrastructure will also provide immediate job opportunities for Rhode Islanders who are working less than they would like and making less than it takes to get by.

Infrastructure investments typically bring higher wages and better quality of life for years in the future. Investing in our public infrastructure – our roads, bridges, schools, ports, and more – creates immediate jobs, makes our communities safer and healthier, and lays the foundation for a brighter future for all Rhode Island families.

]]>